Buying a home in 2026 requires more upfront cash than in recent decades. On a $422,921 home, a 10% deposit means saving $42,292, which is no small amount for most buyers.

With the U.S. median household income at $83,730, saving for a home can feel overwhelming. That’s why having a clear plan is more important than ever.

This guide breaks down exactly how much you need to save and how long it will realistically take. We have mentioned 12 strategies to get you closer to owning your home.

Houzeo is America’s best home buying and selling platform.

For Home Sellers: List your home for a Flat Fee, and save 2.5% to 5.5% on the listing agent commission! That’s thousands of dollars extra in your pocket.

For Home Buyers: Houzeo has the largest number of houses for sale in the US. Start your dream home search now!

Yes! You can list your home for sale or search millions of homes on the Houzeo mobile app!

Download now on the Apple App Store or the Google Play Store.

Key Takeaways

- For a median-priced home of $422,921, your total savings target should fall between $60,900 and $98,100.

- As a first-time buyer, you need to save an average 10% amount of the home’s purchase price.

- A zero-based budget, automated transfers, and a HYSA are the three fastest ways to build your house fund.

- Your DTI needs to stay under 43%. Clear high-interest debt like credit cards before saving, or lenders may not approve your mortgage.

- Eligible buyers can skip the down payment entirely with VA or USDA loans.

How Much Should You Save Before Buying a House?

Before you start saving, you need to understand what costs are associated with buying a house. You need to consider the total cost you need in the bank before you close.

According to the NAR, the median down payment for first-time buyers is 10% and 23% for repeat buyers. The median down payment for all buyers was 19%. That said, the higher the down payment, the lower the mortgage insurance and monthly payments.

Here’s a breakdown of every upfront cost to factor into your savings goal for a US median home price of $422,921:

| Type of Cost | Range | Incurred Cost |

|---|---|---|

| Down Payment | 10% of home price | $42,292 |

| Closing Costs | 2%–6% of your loan amount | $7,600 – $22,800 |

| Moving Costs | $1,000 – $5,000 | $1,000 – $5,000 |

| Immediate Repairs | $1,000 – $3,000 | $1,000 – $3,000 |

| Emergency Buffer | 3–6 months of expenses | $9,000 – $25,000 (est.) |

| Total Savings Target | – | $60,900 – $98,100 |

Note: Closing costs are calculated based on the loan amount, not the home price. At 10% down, your loan is $380,629. So 2%–6% of that runs $7,600–$22,800.

Not everyone buys at the median price, and programs like FHA, VA, and down payment assistance can significantly lower your required down payment.

How Long Does it Take to Save for a House?

Your savings timeline depends on two things: your total target and your monthly savings rate. If you want to know how to start saving money for a house with an achievable deadline in mind, start here.

| Monthly Savings | $43K Goal (DP only) | $60K Goal (DP+Closing Cost+ Minimal Buffer) | $80K Goal (Mid Range) | $100K Goal (With Healthy Emergency Buffer) |

|---|---|---|---|---|

| $1,000/month | 43 mo (3.6 yrs) | 60 mo (5 yrs) | 80 mo (6.7 yrs) | 100 mo (8.3 yrs) |

| $1,500/month | 29 mo (2.4 yrs) | 40 mo (3.3 yrs) | 54 mo (4.5 yrs) | 67 mo (5.6 yrs) |

| $2,000/month | 22 months | 30 months | 40 months | 50 months |

| $2,500/month | 18 months | 24 months | 32 months | 40 months |

You need to save roughly $1,800/month to hit the $43K down payment mark, or $2,500/month to reach the full $60K conservative target. It’s aggressive but achievable. If your saving timeline feels too long, the issue is usually one of two things: your savings rate is too low, or your target is higher than it needs to be.

12 Ways to Save Money for a House Faster

Cutting unnecessary expenses, increasing your income, and automating savings all help. The best results usually come from combining these habits with smart financial planning.

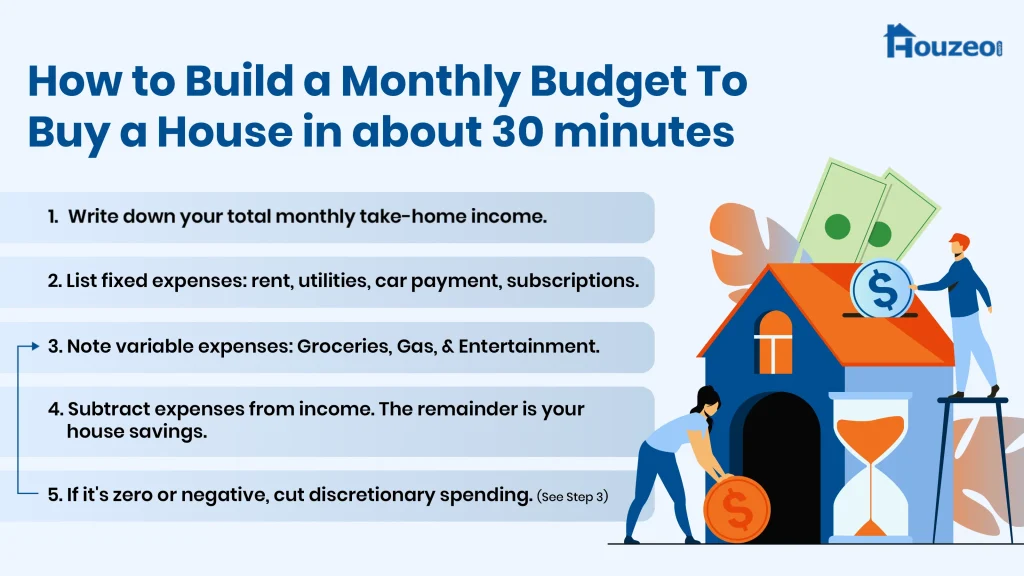

1. Build a Zero-Based Monthly Budget

The best way to save for a house is to know exactly where every dollar goes before the month starts. That’s what a zero-based budget does. It assigns every dollar a job so nothing slips through the cracks.

This approach also provides a starting point for budgeting for a house. Without a clear view of your monthly finances, it’s difficult to set a realistic savings target.

2. Automate Your Savings

Set up an automatic transfer on payday from your checking account to a dedicated house savings account. Move the same amount every time you get paid, so saving becomes automatic.

You’re less likely to spend money that never sits in your checking account. Consider naming the account something like “House Fund” or “Down Payment 2026.” Labeling it makes you less likely to touch it.

3. Open a High-Yield Savings Account (HYSA)

If you’re looking for the best account to save for a house, a HYSA is the right place to start. Standard savings accounts earn next to nothing (under 0.5% APY). Over a 2–3 year period, this difference can add hundreds or even thousands of dollars to your house savings.

HYSA accounts (3.8%–5.0% APY) are FDIC-insured, fully liquid, and ideal for anyone who is looking to save for a house for a time period of 12-36 months. Based on your house saving goals, here’s how the extra interest can grow compared to a standard account at typical rates in 2026:

| Balance | Typical Standard Savings (around 0.5% APY) | High‑Yield Savings (4%–5.0% APY) | Annual Difference |

|---|---|---|---|

| $20,000 | $100/year | $800–$1,000/year | $700–$900 |

| $40,000 | $200/year | $1,600–$2,000/year | $1,400–$1,800 |

| $60,000 | $300/year | $2,400–$3,000/year | $2,100–$2,700 |

| $80,000 | $400/year | $3,200–$4,000/year | $2,800–$3,600 |

Pro Tip If you’re confident you won’t need early access to the cash, a short‑term Certificate of Deposit (CD) can sometimes offer even higher APYs. However, there is a catch. CDs usually restrict withdrawals and can penalize you for early access.

4. Cut Discretionary and Recurring Expenses

Go through your last 3 to 6 months of bank statements and look for opportunities to trim. Focus on:

- Unused subscriptions, like streaming services or gym memberships.

- Eating out more than 2–3 times per week.

- Impulse purchases over $50.

- Auto-renewals on tools or services you rarely open, like online courses or website hosting

Cancel or pause anything non-essential during your “saving to buy a house” period. Even freeing up $150 per month saves $1,800 a year. Instead of calculating in your head, write down the specific subscriptions you’ll cancel this week instead of keeping vague intentions.

5. Consider Downsizing Temporarily

If you plan to buy within 1–2 years, moving to a cheaper rental can free up real cash each month. Lower rent, smaller utility bills, and less upkeep will translate to increased house savings directly.

One year in a smaller or more affordable rental apartment can add $3,000–$10,000 to your savings. It’s a short-term trade with a clear timeline, making it one of the simplest ways to accelerate your saving for a house.

6. Ask for a Raise or Negotiate a Promotion

One of the fastest ways to increase your monthly savings is to earn more. So, if you want to boost your income and haven’t asked for a raise in the past year or more, now would be the right time to knock on your manager’s door.

E.g., a 5% raise on the U.S. median household income of $83,730 adds roughly $4,186 per year, which is close to $349 extra per month.

7. Pick Up a Side Hustle

Wondering about how to save money quickly for a house? Here are some reliable options to consider for extra earnings:

- Rideshare driving like Uber or Lyft

- Delivery driving with services such as DoorDash, Instacart, or Amazon Flex

- Freelance work related to writing, design, coding, and bookkeeping

- Selling unused items on Facebook Marketplace, eBay, or Poshmark

- Waitering part-time at local or major food outlets

- Tutoring or teaching online

Gig work like delivery or rideshare driving typically earns $15–$25 per hour gross, depending on your city and schedule.

8. Rent Out a Room, Car, or Parking Space

You may already own assets that can help you save money to buy a house.

- Spare room: List it on Airbnb or Furnished Finder. Depending on location and occupancy, a room can earn $500–$1,200 per month.

- Car: Rent it out on Turo when you’re not using it. Many owners earn $300–$700 per month.

- Parking space: If you live near a transit stop or busy area, platforms like SpotHero can generate $150–$400 per month.

9. Save Every Windfall

A windfall is any unexpected money, such as a tax refund, work bonus, birthday cash, inheritance, or cashback payout. The average U.S. tax refund in 2025 is about $3,167. Redirecting two or three windfalls each year can cut down several months off your timeline.

10. Skip Large Purchases During Your Saving Window

Decide on a defined savings period – 12, 18, or 24 months. During that time, pause large discretionary spending, such as:

- A new car, unless your current one stops working

- Expensive vacations

- New furniture for a rental you plan to move out of

- Major tech or clothing upgrades

- Annual streaming subscriptions or gym memberships

11. Pause Extra 401(k) Contributions

If you contribute above your employer match to a 401(k), consider temporarily pausing extra contributions above the match and redirecting that money to your house fund for 12–18 months.

Never stop contributing enough to capture your full employer match because that’s free money. It is also better not to withdraw from existing retirement accounts; tax penalties make that a losing trade every time.

12. Adjust Your Tax Withholding

If you get a large tax refund each year, you’ve likely been overpaying taxes and waiting to get your own money back in April. The average 2025 refund was about $3,167, which could have been earning interest in your high-yield savings account all year.

If you consistently overpay, adjusting your W‑4 reduces withholding and puts extra cash into your paycheck each month. On a $3,167 annual refund, that’s roughly $264 per month, money you can automate straight into your home savings bank account.

How to do it:

- Use the IRS Tax Withholding Estimator. It’s free and takes approximately 10 minutes.

- Fill out a new W‑4 and submit it to your HR or payroll department.

- Set up an automatic transfer for the extra monthly amount straight to your house savings account.

Note: This applies to W-2 employees only. If you’re self-employed or usually owe taxes at filing, consult a tax advisor before making changes.

Don’t Just Browse. Buy.

Your entire home purchase, managed in one place.

Download the Houzeo Mobile AppShould You Pay Off Debt or Save for a House First?

Not all debt is equal, and dealing with debt is more than a binary choice. The right answer depends on what kind of loan you’re carrying and what your debt-to-income (DTI) ratio looks like.

When to Pay Off Debt First

Paying down debt in the following situations is the fastest path to mortgage eligibility. It’s not a detour, it’s the route. Hence, prioritize debt if:

- You carry high-interest credit card debt (15%–25% APR). You generally can’t out-save interest at this level.

- The DTI ratio is above 43%. Most lenders won’t approve a mortgage beyond this without things like a high down payment.

- Your monthly minimums leave nothing left to save.

When It’s Okay to Save While Carrying Debt

When your HYSA interest rate and your debt rate are close, carrying that debt while saving is roughly a break-even or financially neutral. Meanwhile, don’t forget, you’re still building your down payment.

You can save and carry debt at the same time if:

- Debt is low-interest (student loans at 4%–6% or a car loan).

- DTI is under 36%.

- Monthly minimums are manageable alongside your savings contributions.

How DTI Affects Your Savings

Before you start saving, it’s important to understand your Debt-to-Income (DTI) ratio. Your debt-to-income (DTI) ratio shows the portion of your monthly income that goes to debt payments for credit cards, student loans, and car payments.

DTI = Total Monthly Debt Payments ÷ Gross Monthly Income

For e.g, $2,000 ÷ $6,000 = 33% DTI

Lenders use DTI to decide:

- Can they safely lend you a mortgage?

- How much will you need for a down payment?

- What interest rate will they offer?

| DTI Range | Meaning for Mortgage Approval |

|---|---|

| Under 36% | Likely approval with the best rates and most loan options |

| 36%–43% | Acceptable. Most lenders approve, may face slightly higher rates |

| 43%–50% | Difficult. Approval depends on strong credit, a larger down payment, or other compensating factors |

| Above 50% | Most lenders will decline. Reducing debt first is usually necessary |

Tip Consult a mortgage lender to determine the best down payment strategy for your financial goals.

How Your Credit Score Affects How Much You Need to Save

Your credit score doesn’t just influence your interest rate; it also changes how much you’ll need to save for a down payment. Different loan programs have different minimum scores and down payment requirements. Here’s what that looks like with the median U.S. home price of $422,921.

| Loan Type | Minimum Credit Score | Minimum Down Payment | Amount to Save |

|---|---|---|---|

| Conventional | 620+ | 3% (income limits apply) or 5%–20% | $12,688 |

| FHA | 580+ | 3.5% | $14,802 |

| FHA (lower) | 500-579 | 10% | $42,292 |

| VA | 620+ | 0% | $0 |

| USDA | 640+ | 0% | $0 |

Note A lower credit score can force you to increase your savings even before you can qualify for a mortgage, and that’s in addition to any impact on interest rates.

Quick Wins to Improve Your Score While Saving

Many buyers can reach 580+ for an FHA or 620+ for a conventional loan within 3–6 months by taking the following steps:

- Keep credit card balances below 30% of your limit to raise your score 20–50 points.

- Pay every bill on time. Even a single missed payment can hurt your score.

- Avoid opening new credit accounts during your saving period.

- Don’t close old accounts since credit history length matters.

- Check your free credit report and dispute any errors.

Loan Programs and Mortgage Down Payment Savings Strategies

If you’re figuring out how to save money for a house, you may not need to save as much as you think. Several programs exist to reduce what eligible buyers need upfront. Simple mortgage tips can also help you make the most of these programs and shorten your savings timeline.

Conventional Loans – 3% Down

Standard mortgages are not backed by the government. Fannie Mae’s HomeReady and Freddie Mac’s Home Possible both allow 3% downpayment. However,

- It requires a 620+ credit score.

- PMI applies until you reach 20% equity, but it can be removed later.

- Good option for buyers with solid credit who want flexibility.

Federal Housing Administration (FHA) Loans – 3.5% Down

FHA Loans are the most common loans for first-time buyers, which require,

- 3.5% down with a 580+ credit score.

- 10% down if your score is 500–579.

- Mortgage Insurance Premium (MIP) applies for the life of the loan if you put less than 10% down.

Veterans Affairs (VA) Loan – 0% Down

VA Loans are available for active military personnel, veterans, and eligible surviving spouses and require,

- No down payment.

- No PMI.

- Competitive interest rates.

United States Department of Agriculture Loans (USDA) Loans – 0% Down

USDA Loans are given for homes in eligible rural and suburban areas. That said, some requirements for the USDA are:

- No down payment needed.

- Income limits are typically up to 115% of the area median income.

- Property must be in a USDA-eligible location.

- Most lenders require a 640+ credit score.

Down Payment Assistance (DPA) Program

DPA program grants or low-interest loans from state and local governments that cover part or all of your down payment. Some of the highlights include:

- Some DPAs are outright grants. So, no repayment is required.

- Eligibility varies by state, income, and property type.

- If you qualify, this is one of the most effective ways to reduce your savings target.

How FSBO + Flat-Fee MLS Can Cut Your Total Housing Cost

Most buyers focus entirely on saving for a down payment. However, if you’re also selling a home to fund your next purchase, real estate commissions can quietly reduce the cash you keep.

Since the National Association of Realtors settlement, commission rates are fully negotiable. Total commissions still commonly range from 2.5%–6%, depending on your market and the agreement you reach. On a $422,921 home, a 5.5% total commission equals about $23,261, with roughly half ($11,630) going to the buyer’s agent.

Selling FSBO (For Sale By Owner) lets you skip the listing agent commission entirely. Meanwhile, a flat-fee MLS listing service like Houzeo lists your home on the MLS, let your manage the sale yourself, and allows you to keep most of the commission savings.

| Sale Price | Comission at ~5.5% | Buyer Agent Commission ~2.75% | Flat-Fee MLS Listing* |

|---|---|---|---|

| $300,000 | $16,500 | $8,250 | $100 – $1,000 |

| $422,921 | $23,261 | $11,630 | $100 – $1,000 |

| $600,000 | $33,000 | $16,500 | $100 – $1,000 |

When to Get Mortgage Preapproval

You can apply for mortgage preapproval after your savings and credit score are in a qualifying range. It helps you budget for a house purchase before touring homes. With preapproval, you are more likely to be preferred by sellers, since the financing has already been reviewed.

Preapproval decisions typically come back within 1–3 business days. Preapproval letters are usually valid for 60–90 days. However, if your search takes longer, you can request a refresh.

Documents mortgage lenders ask:

- Last two years of W-2s or tax returns

- Pay stubs from the last 30 days

- Two to three months of bank statements

- Government-issued ID

- Details of outstanding debts (student loans, auto loans, credit cards)

Get Pre Approved for a Mortgage🏡

Select Your Loan Type

-

New Home Purchase

New Home Purchase

-

Mortgage Refinance

-

Cash-out Refinance

So, How Can I Save For a House?

Start with a zero-based budget and automate your savings from day one. Open a HYSA to grow your fund faster and cut recurring expenses. If you’re also selling a home, going FSBO with a flat-fee MLS listing can save tens of thousands in commission.

» Houzeo Reviews: Read what customers have to say about Houzeo, America’s best home buying website.