For households headed by people ages 24 to 32, the homeownership rate dropped from 45% in 2005 to 36% in 2014. Many economists pointed to rising student loan debt as one possible reason, since it can make home ownership harder for young borrowers.

Student loan debt doesn’t have to stand in the way of home ownership. In fact, the Federal Reserve has found that while student debt can delay it, many young adults still become homeowners.

Houzeo is America’s best home buying and selling platform.

For Home Sellers: List your home for a Flat Fee, and save 2.5% to 5.5% on the listing agent commission! That’s thousands of dollars extra in your pocket.

For Home Buyers: Houzeo has the most number of houses for sale in US. Start your dream home search now!

Yes! You can list your home for sale or search millions of homes on the Houzeo mobile app!

Download now on the Apple App Store or the Google Play Store.

Key Takeaways

- Student loan debt doesn’t automatically stop you from buying a home: Lenders evaluate your overall finances, not just your student loans.

- Lenders focus on key financial factors: Your debt-to-income ratio, credit score, income, and monthly payments determine eligibility.

- Multiple loan options are available: FHA, conventional, and VA loans can all work for buyers with student debt.

- A stronger financial profile improves approval chances: Better credit, stable income, and lower debt increase your chances.

- Paying off student loans first is not always required: Many buyers qualify for a mortgage while still repaying their loans.

Can You Buy a House With Student Loans?

Yes, you can buy a house with student loan debt. Having student loans may affect how much you can borrow, but it does not automatically disqualify you from home ownership.

With the right lender, a strong credit profile, and a manageable debt-to-income ratio, many buyers still qualify for a mortgage.

Do Student Loans Affect Buying a House?

Student loans can influence mortgage approval mainly by affecting your monthly debt load. Lenders look at how much of your income goes toward debt payments, your credit score, and your overall financial stability.

1. Debt-to-Income Ratio (DTI)

Your debt-to-income ratio compares your monthly debt payments to your monthly income. A lower DTI usually improves your chances of getting approved because it shows lenders that you can handle another monthly payment.

2. Student Loans and Buying a House: Credit Score Impact

Student loans can also affect your credit score, especially if you miss payments or carry high balances. On the other hand, making payments on time can help show lenders that you are a responsible borrower. The first step every lender takes to verify your creditworthiness is a credit check.

3. Income & Repayment Plans

Your income and repayment plan matter too. A borrower with a steady income and an income-driven repayment plan has a better chance to qualify for a mortgage.

Loan Options for Buying a Home With Student Loans

If you plan to buy a home with student loan debt, getting a mortgage with a student loan depends on your credit, savings, and debt load.

1. Conventional Loans: These loans are often best for buyers with stronger credit scores and manageable debt levels. Keeping your DTI ratio under control can improve your chances of approval, though mortgage insurance may still be required in some cases.

2. VA Loans: VA loans are often a strong option for eligible veterans, active-duty service members, and some surviving spouses since they typically require no down payment and can offer favorable terms.

3. USDA Loans: USDA loans require your DTI ratio to typically stay at or below 41%. Higher ratios may be allowed with strong compensating factors like higher credit scores or stable income. For student loans, lenders use your actual monthly payment

4. FHA Loans: FHA loans can be a good fit for borrowers with limited savings because they usually offer flexible credit standards and lower down payment requirements. FHA student loans also consider Income-Driven Replacement (IDR).

Income-Driven Repayment (IDR) plans adjust federal student loan payments based on your income and family size, typically capping them at 10-20% of discretionary income (above 150% of the poverty line). After 20-25 years of qualifying payments, any remaining balance is forgiven.

| Loan Type | Down Payment | Credit Score | DTI Ratio | Mortgage Insurance | Best For |

|---|---|---|---|---|---|

| FHA | 3.5% | 580+ | Up to 50% | Required | Buyers with lower credit or smaller savings |

| Conventional | 3% | 620+ | Up to 45% | Required if down payment is under 20% | Buyers with stronger credit and stable income |

| VA | 0% | No official minimum, 620 standard | Up to 41% | Not required | Eligible veterans and service members |

| USDA | 0% | No official minimum, 640 standard | Up to 41% | Guarantee fee required | Buyers in eligible rural areas |

Student loan forgiveness cancels some or all of your remaining federal loan balance after meeting certain conditions.

The two most common programs are Public Service Loan Forgiveness (PSLF), which forgives your balance after 10 years of qualifying payments in public service, and Income-Driven Repayment (IDR) forgiveness, which cancels the remaining balance after 20–25 years of income-based payments.

For mortgage purposes, being on a forgiveness track can work in your favor because IDR payments are typically lower, which can improve your DTI. However, lender policies vary; some count only your current monthly payment while others factor in the full remaining balance.

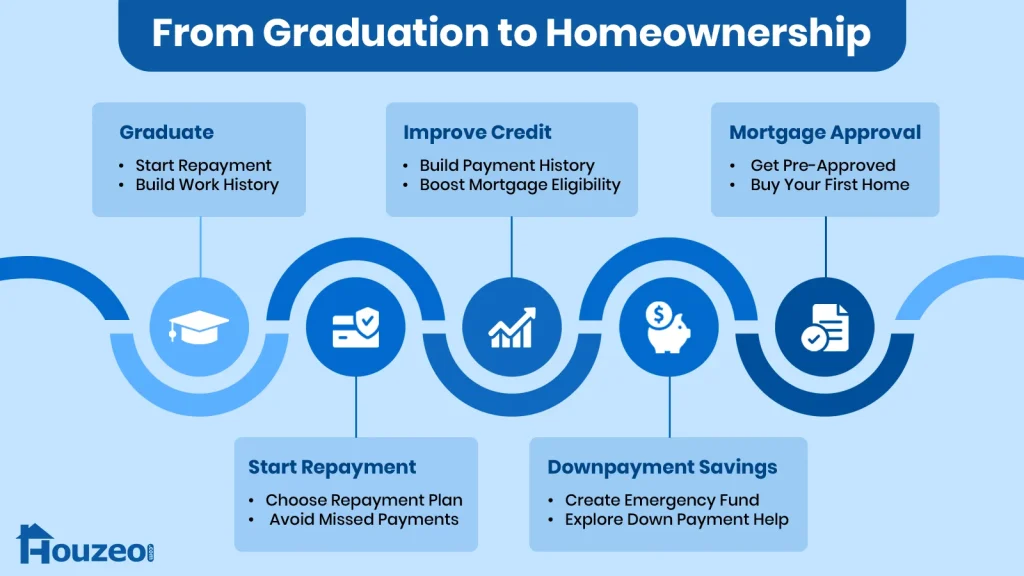

How Can I Buy a House with Student Loan Debt?

Before you start looking for homes for sale, get your finances in order so you know exactly where you stand.

A few small improvements in your credit, debt, and income can make a big difference in how much home you can afford. It can also affect how smoothly the mortgage process goes for buying a house with student loan debt.

1. Calculate Your DTI

- Add up all your monthly debts: Include student loans, credit cards, car loans, and any other recurring obligations to get a clear total.

- Divide by your gross monthly income: This calculation gives you your debt-to-income ratio.

- Lenders rely on this number: It helps them determine whether you can handle a mortgage along with your existing debt.

- A lower DTI improves your chances: It can increase approval odds and may help you qualify for better loan terms.

Quick Tip If your DTI or credit score is holding you back, adding a co-borrower such as a spouse, partner, or family member can strengthen your application. Lenders will combine both incomes, which can improve your DTI significantly.

2. Improve Your Credit Score

- Check your credit report for errors: Review it carefully and dispute any inaccurate information that could lower your score.

- Pay all bills on time: Payment history is a major factor, and consistently paying on time helps build strong credit.

- Keep credit card balances low: High balances can hurt your credit utilization ratio and reduce your score.

- Avoid opening new credit accounts: New accounts before a mortgage application can negatively impact your profile.

- Even small improvements make a difference: A slight credit score improvement can expand your loan options and improve terms.

3. Reduce Your Debt

- Pay down high-interest debt first: Focus on credit cards and personal loans to reduce costly interest and financial strain.

- Lower your student loan burden if possible: Making extra payments can reduce your monthly obligations over time.

- Avoid taking on new debt: New loans before buying a home can hurt your mortgage eligibility.

- Fewer debts improve your DTI: Reducing obligations lowers your debt-to-income ratio and boosts chances to qualify for a mortgage.

- Lower monthly payments reduce lender risk: Smaller debt commitments make you a more reliable borrower in the eyes of lenders.

4. Increase Your Income

- Ask for a raise if possible: If your performance supports it, a higher salary can strengthen your financial profile.

- Consider a side hustle or freelance work: Extra income streams can boost your monthly earnings.

- Look for better job opportunities: Higher-paying or more stable roles can improve your long-term affordability.

- More income increases buying power: It can help you qualify for a larger mortgage and manage payments more comfortably.

5. Get Pre-Approved

- Reach out to a lender early: Start the process before house hunting to understand your financial position.

- Submit your financial details: Share your income, debt, credit, and employment information for review.

- Pre-approval defines your budget: If you get pre-approved, it shows the seller that you’re serious about the purchase and how much home you may be able to afford.

- It strengthens your position as a buyer: You can shop confidently within budget and appear more credible to sellers.

Pro Tip When using a mortgage calculator, don’t just enter the home price; slightly increase the interest rate by 0.5%–1% to estimate a realistic monthly payment and avoid overextending your budget when buying a house with student loans.

Buying a Home With Student Loan Debt: Different Loan Amounts

The amount of student loan debt you have can affect how much house you can afford, but it does not automatically decide whether you can buy.

Lenders care more about your monthly payment, income, credit score, and debt-to-income ratio than the total balance alone.

$50K Student Loan

At this amount, monthly payments on a standard 10-year plan typically fall around $500–$550. For most buyers with limited additional debt, this leaves enough room in the budget to include a mortgage payment.

First-time buyers in this range often find FHA loans particularly accessible. The lower down payment requirement means less cash tied up upfront while still carrying student debt.

$100K Student Loan

Payments here can be up to $1,000–$1,100 on a standard plan, which puts more noticeable pressure on your DTI. If that feels tight, you can switch to an IDR plan before you apply. This can bring your monthly obligation down significantly and improve your approval odds.

Buyers in this range also benefit from building a stronger credit profile beforehand. A higher score can offset some of the DTI concern in a lender’s eyes, especially in a conventional loan.

$200K Student Loan

Standard monthly payments can exceed $2,000, which makes this the most demanding scenario for lenders. Approval is still possible, but it typically requires a combination of high, stable income and minimal other debts.

An IDR plan becomes almost essential here, as it can reduce your monthly payment to a fraction of the standard amount. If your DTI is still too high after adjusting your repayment plan, a more flexible loan program or a larger down payment may help.

Quick Tip Home loans require considerable down payments up front. In addition, if you want to avoid Private Mortgage Insurance (PMI), you have to pay a 20% down payment up front.

Should I Pay Off Student Loans Before Buying a House?

Not always. Paying off student loans before buying a house can help if it lowers your monthly debt payments enough to improve your DTI ratio.

But if your loans are already on manageable terms and you are otherwise ready to buy, waiting to become debt-free may delay homeownership more than necessary.

| Pay Off Student Loans First 💸 | Buy a House First 🏡 |

|---|---|

| Your monthly student loan payments are high. | Your monthly payments are low and manageable. |

| Your debt-to-income ratio is too high for mortgage approval. | Your DTI is within the acceptable range for most lenders. |

| Your credit score has taken hits from missed or late payments. | Your credit score is strong and mortgage-ready. |

| You have little to no savings for a down payment. | You have enough saved for a down payment and closing costs. |

| Renting is affordable and does not strain your budget. | Renting costs are high enough that owning makes more financial sense. |

| Your income is unstable or irregular. | You have a stable, reliable source of income. |

Should You Buy a House After Student Loan Debt?

You can buy a house with student loans; it’s not a barrier, but simply a part of your financial picture. While debt affects your mortgage application, lenders focus on your DTI, credit score, and income stability, not just your total loan balance.

By improving your credit, managing your debt wisely, and exploring the right loan options, you can successfully buy a home even with student loan debt.

» Houzeo Reviews: Read what customers have to say about Houzeo, America’s best home buying website.