Foreclosure activity climbed again in 2025, with 367,460 U.S. properties entering foreclosure filings that year. As housing costs went up, distressed properties continue to attract buyers looking for lower entry prices and better value.

That’s why HUD homes and other foreclosure-related listings remain worth watching for anyone hoping to buy below market value. Buying a home below market value sounds appealing, but not every buyer understands how HUD homes actually work.

If you’re considering one, it’s important to understand not just what a HUD home is, but how it works and what to look out for before making a decision.

Houzeo is America’s best home buying and selling platform.

For Home Sellers: List your home for a Flat Fee, and save 2.5% to 5.5% on the listing agent commission! That’s thousands of dollars extra in your pocket.

For Home Buyers: Houzeo has the most number of houses for sale in US. Start your dream home search now!

Yes! You can list your home for sale or search millions of homes on the Houzeo mobile app!

Download now on the Apple App Store or the Google Play Store.

Key Takeaways

- HUD homes are often priced below market value: These properties are sold after foreclosure, so the goal is to recover the loan balance rather than maximize profit.

- Owner-occupants get priority when bidding: HUD gives preference to buyers who plan to live in the home, limiting investor competition in the initial listing period.

- You must work with a HUD-approved agent: Buyers cannot submit bids on their own and need a registered agent to place offers through the HUD system.

- Financing should be ready before bidding: Since HUD follows strict timelines and some homes may not qualify for all loan types, pre-approval is essential.

- HUD homes are sold as-is: The government does not make repairs, so inspections help uncover the true condition and potential costs early.

- HUD homes follow a strict bidding process: Offers are reviewed during specific deadlines, and the highest acceptable bid is selected based on price and buyer eligibility.

What Does HUD Stand For?

HUD stands for the Department of Housing and Urban Development. If you’re wondering what does HUD stand for in real estate, it refers to the federal agency that oversees housing programs and promotes homeownership in the United States.

It plays a key role in managing FHA loans, which are directly linked to HUD foreclosed homes and repossessed HUD homes. HUD homes can be a practical way to buy a house at a lower price, but only if you understand how they work.

These homes are government-owned properties that are resold after a borrower defaults on an FHA loan. Because the goal is to recover losses, they are often priced competitively. A HUD home is a property the government takes ownership of after a borrower defaults on an FHA loan.

It starts when a buyer purchases a home using an FHA loan. If the borrower defaults on payments, the lender forecloses and files a claim with HUD. The property is then transferred to the government, which lists it for sale to recover the loan amount.

HUD Homes vs HUD Housing

HUD homes and HUD housing sound similar, but serve very different purposes. One offers properties for purchase, the other provides rental and assistance programs.

| Aspect | HUD Homes | HUD Housing |

|---|---|---|

| Definition | Foreclosed single-family properties sold by HUD after FHA loan defaults | Broader programs like Section 8 vouchers, public housing rentals, and subsidies for low-income residents |

| Property Type | Individual homes sold “as-is” via auctions | Multi-unit apartments or rental assistance |

| Buyer/Renter | Owner-occupants and investors bid online | Eligible low-income families, seniors, disabled |

| Priority | Owner-occupants first, then investors | Income-based eligibility, no ownership focus |

| Cost Structure | Often below-market prices, buyer pays repairs | Subsidized rents (30% of income typical) |

| Access | HUDHomeStore.gov listings with deadlines | Local housing authorities manage applications |

Why are HUD Homes popular? HUD homes are typically priced to sell, which is why they often attract first time home buyers and investors.

What to Check Before Buying a HUD Home

Before submitting a bid, evaluate these factors carefully. While HUD homes can offer savings, missing key details can lead to higher long-term costs.

Property Condition

HUD foreclosure homes are sold “as-is,” meaning the government will not make any repairs before the sale.

- Inspect for structural issues like foundation cracks, roof leaks, or water damage. These repairs can be costly and may affect the home’s long-term value.

- Pay close attention to major systems, including electrical wiring, plumbing, and HVAC. Outdated or damaged systems can significantly increase your upfront expenses after purchase.

- Always review the Property Condition Report (PCR), if available. It provides a snapshot of the home’s condition and can help you identify potential problems before moving forward.

Estimated Repair & Renovation Costs

- A lower listing price can be misleading if repair costs are high, especially with foreclosure properties. What looks like a bargain upfront can quickly become expensive once renovation work begins.

- Before placing a bid, try to get rough estimates from contractors. Even ballpark figures can give you a clearer picture of how much you’ll actually need to invest.

- Factor in essential repairs such as roofing, flooring, and plumbing. These are not cosmetic fixes—they’re necessary for the home to be livable and safe.

- It’s also smart to add a 10–20% buffer for unexpected repairs. Hidden issues often surface after purchase, particularly in “as-is” homes.

- Finally, compare your total investment purchase price, including repair costs, with nearby home values. This helps ensure you’re not overpaying and that the deal still makes financial sense.

Compare the total investment, including the price and repair costs, with nearby home values to ensure you’re not overpaying.

Local Market Value

- Analyze recent sales: Study recently sold homes in the same area to understand the true market value and what buyers are currently paying.

- Compare price per square foot: Measure the property against similar HUD modular homes to see if the pricing is fair based on size and layout.

- Evaluate property condition: Factor in the home’s current state, needed repairs, and any upgrades, as these directly impact overall value.

- Assess neighborhood demand: Look at location quality, nearby amenities, and market trends to gauge future appreciation and desirability.

- Calculate total investment: Add purchase price and estimated repair costs, then compare with nearby home values to ensure you’re not overpaying.

Financing Readiness

- Pre-approval is essential: Get pre-approved for a mortgage (FHA or conventional) before bidding to show you’re a serious buyer.

- Have funds ready: Ensure your down payment and closing costs are available to avoid last-minute delays.

- Check financing eligibility:

Confirm the property qualifies for your HUD loan type, as some homes may need repairs before approval. - Act within strict timelines: HUD transactions move quickly, so any financing delay can result in losing the deal.

Bidding Process & Deadlines

HUD homes are sold through a structured bidding system rather than traditional negotiation.

- HUD homes use a structured bidding system: Unlike traditional home sales, there is no back-and-forth negotiation, so buyers must follow strict timelines and submit competitive offers.

- Pay close attention to bid deadlines: HUD reviews offers within specific periods, and missing a deadline can mean losing the opportunity.

- Understand the owner-occupant priority period: Homes are first offered to buyers who plan to live in the property before investors can participate.

- Submit your highest and best offer upfront: Since counteroffers are rare, putting forward a strong initial bid improves your chances of acceptance.

Title & Legal Status

Although HUD homes typically come with clear titles, due diligence is still essential.

- Check for liens or unpaid taxes: Outstanding debts tied to the property can create complications if not identified early.

- Review title insurance options: Check title insurance to protect against potential ownership disputes or claims after purchase.

- Confirm all legal documents before closing: Ensuring accuracy in paperwork helps avoid delays or unexpected issues during the final transaction.

Neighborhood & Location Factors

The surrounding area plays a major role in a property’s long-term value, sometimes even more than the home itself.

Look into nearby amenities, schools, public transport, and overall connectivity. Easy access to essentials like grocery stores, hospitals, and major roads can significantly improve both livability and future value.

It’s also important to review crime rates and broader neighborhood trends. Areas with improving infrastructure or new developments often see stronger appreciation over time.

Finally, evaluate the property’s resale potential or rental demand. A home in a desirable location is easier to sell later and can generate steady income if you decide to rent it out.

Pro Tip When comparing HUD homes, don’t just chase the lowest price; look for the best places to live with strong demand, good schools, and stable resale potential, so your “deal” still makes sense after repairs and closing costs.

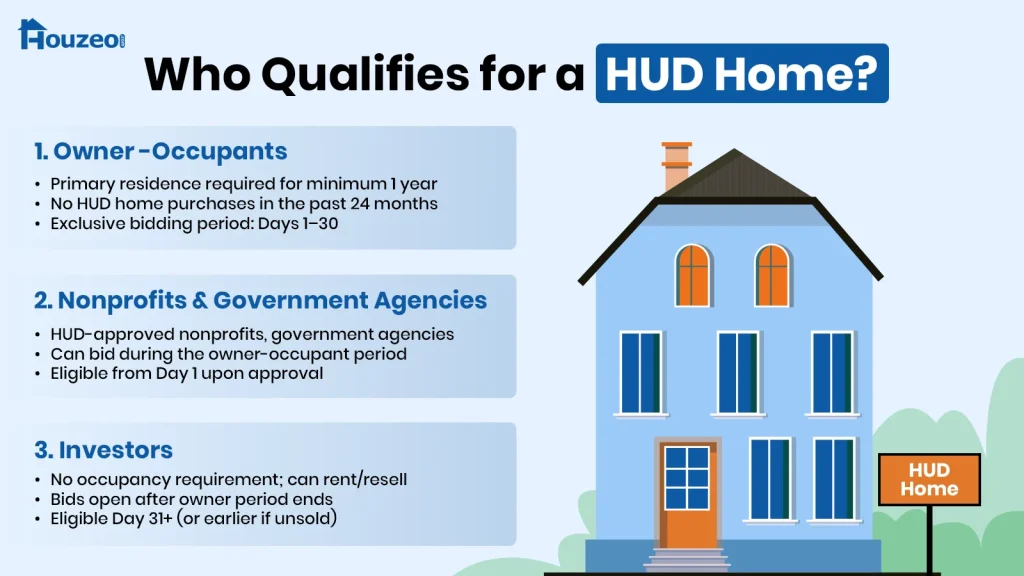

Who Qualifies for a HUD Home?

HUD homes are open to several types of buyers, but the bidding order and eligibility rules change depending on who is applying.

Eligibility for HUD Housing:

- Owner-occupant priority: Buyers who intend to live in the home get exclusive access during the initial bidding period, increasing their chances of winning the bid.

- Investor eligibility: Investors can participate only after the owner-occupant phase ends, and only if the property is still unsold.

How to Buy a HUD Home

Buying a HUD home involves a structured process that differs from traditional home purchases. Understanding each step can help you avoid delays and improve your chances of success.

Step 1: Search for HUD Homes

Start by browsing listings on HUD HomeStore, HUD.gov’s homes-for-sale page, or other real estate sites that feature HUD properties.

- Check the listing status: Every HUD listing displays one of three statuses, Exclusive (owner-occupants only), Extended (all buyers including investors), or Lottery (random selection from tied bids).

- Understand condition codes: HUD labels each property as Insured (IN), Insured with Escrow (IE), or Uninsured (UI). IN homes are move-in ready and eligible for standard FHA loans.

- Note the case number: Each HUD listing has a unique case number. Save it as your agent will need it when submitting your bid through the portal.

- Track days on market: Listings that have been active for a while may have dropped in price. If they moved from Exclusive to Extended status, they signal more room to negotiate.

Step 2: Work With a HUD-Approved Agent

You cannot submit a bid directly to HUD; all offers must go through a HUD-registered real estate broker.

- Confirm active registration: Not every licensed agent is registered with HUD. Ask specifically whether they are currently active in the HUD system.

- Look for HUD transaction experience: An agent who has closed HUD deals before knows how to calculate net bids correctly and navigate the portal without errors.

- Know how their commission works: HUD pays the buyer’s agent commission directly, typically up to 3% of the purchase price.

- Sign a buyer representation agreement: It formalizes the relationship and clarifies each party’s responsibilities before the bidding process begins.

Step 3: Submit Your Bid

Once you’ve identified a property, your agent submits your offer through the HUD HomeStore portal during the active bidding window.

- Understand how net bids work: HUD selects the highest net bid, not the highest gross offer. The net bid is your offer price minus any closing cost assistance or agent commission.

- Submit only once per bidding period: HUD allows one bid per buyer per property per period..

- Respond to acceptance within 24–48 hours: If HUD accepts your bid, you must pay the earnest money deposit almost immediately.

- Expect a response within 1–3 business days: HUD notifies buyers of acceptance, rejection, or counter-offer through the portal.

Step 4: Complete Your Inspection

After bid acceptance, you enter the inspection period, typically 15 days. This is your only opportunity to assess the property before committing fully.

- Book your inspector immediately: Contact a licensed home inspector the same day your bid is accepted so you’re not scrambling near the deadline.

- Add a pest/termite inspection: Standard home inspections don’t cover wood-destroying organisms. For older or long-vacant properties, a separate pest report can catch costly hidden damage.

- Use the inspection to make a go/no-go decision: If serious issues surface, you can withdraw during the inspection period and receive your earnest money refund. HUD homes are sold as-is, but some buyers still arrange inspections if the property allows it.

Step 5: Secure Final Loan Approval

With the inspection complete and your decision made to proceed, shift focus entirely to getting your loan across the finish line before HUD’s closing deadline.

- Submit all lender documents immediately: Your lender will need pay stubs, bank statements, tax returns, and the signed purchase contract.

- Prepare for the appraisal: Your lender will order an appraisal to confirm the property value supports your loan amount.

- Confirm your cash to close: Calculate your exact down payment plus closing costs ahead of time and make sure those funds are there in your account.

Step 6: Close the Deal

Owner-occupants typically have 45 days from bid acceptance to close; cash buyers often close in 20–30 days. Missing HUD’s deadline forfeits your earnest money deposit.

- Review the Closing Disclosure carefully: You’ll receive this document at least three business days before closing.

- Do a final walkthrough: Walk through the property one last time before closing to confirm its condition matches what you saw during inspection.

- Sign and receive keys: At closing, you’ll sign the loan and transfer documents, pay your down payment and closing costs, and take ownership.

- Listing price and bidding deadline: Shows the property’s price and how much time you have to submit an offer. HUD homes follow strict timelines, so acting quickly is important.

- Property condition details: Provide an overview of the home’s current state, including visible issues or general wear and tear.

- Repair disclosures: If available, these highlight known problems and help you estimate renovation costs more accurately.

- Buyer eligibility: Specifies whether the property is open to owner-occupants, investors, or both.

- Owner-occupant priority: Owner-occupants are given priority during the initial bidding period before investors can submit offers, improving their chances of securing the property.

Financing Options for HUD Homes

Several financing options are available depending on the property condition and buyer eligibility.

- FHA loans: They are a good fit for buyers who want a lower down payment and have more flexible credit requirements.

- FHA 203(k) loans: They are useful when the home needs repairs, since they let you finance both the purchase price and renovation costs in one loan.

- Conventional loans: They may work best for HUD homes that are in relatively good condition and need only minor repairs.

- Cash purchases: These can be faster and simpler, especially when the property has issues that make financing harder.

- HUD loan requirements: Some foreclosed HUD houses may not qualify for every loan type, so buyers should confirm loan eligibility early in the process.

What Are HUD’s Incentive Programs?

HUD offers several incentive programs to make home ownership more accessible and to encourage buyers to purchase HUD-owned properties.

These programs can reduce the upfront cost of buying a home and, in some cases, provide special pricing or down payment benefits for eligible buyers.

- Good Neighbor Next Door: This program is designed for public servants such as teachers, firefighters, law enforcement officers, and emergency medical technicians. Eligible buyers may receive a 50% discount off the list price of a HUD home in a revitalization area.

- Dollar Homes Program: This program allows local governments to purchase certain HUD homes for just $1, usually when the property has been listed for an extended period and needs significant attention.

- HUD Nonprofit Program: HUD-approved nonprofit organizations may be able to buy certain homes at a discount, often up to 30%, to support affordable housing efforts.

- Housing Choice Voucher Program: In some cases, this program can help eligible renters transition into homeownership by lowering the down payment requirement, including access to options as low as $100 on select HUD homes.

What Are Pros and Cons of HUD Home?

✅ Pros of Buying a HUD Home

- HUD homes are often sold below market value because they are foreclosure properties.

- Owner-occupants usually get priority during the initial bidding period, which gives regular homebuyers a better chance than investors.

- HUD may offer closing cost assistance of up to 3% if the buyer meets program requirements.

- Some buyers may qualify for low down payment options under certain Housing and Urban Development programs.

- HUD properties are listed publicly, making them easier to find and compare than many private distressed sales.

- HUD homes can be a good entry point for first-tim

- e buyers looking for lower upfront costs.

- There may be room for equity growth if the home is purchased at a discount and improved over time.

❌ Cons of Buying a HUD Home

- HUD homes are sold as-is, so the buyer usually cannot ask the seller to make repairs before closing.

- The home may need major repairs since the previous owner likely struggled to maintain the property.

- Buyers must work with a HUD-approved real estate agent, which adds an extra step to the process.

- The bidding process can be slow and highly structured, which may not suit buyers who want a faster purchase.

- Competition can still be strong in affordable markets, especially for well-located properties.

- Owner-occupants are generally expected to live in the home for at least one year after purchase.

- If the owner-occupancy rule is broken, the buyer may lose eligibility to purchase another HUD home for a certain period.

Should I Buy a HUD Home?

A HUD home can be a smart choice if you’re looking to buy a house at a lower cost compared to traditional listings. These homes are usually available on the official HUD website. All you need is a HUD-approved real estate agent to place a bid on your behalf.

However, many HUD homes are sold as-is, which means they may require repairs or renovations to become fully livable. In some cases, it might not be worth the investment. So, it’s highly recommended to get a home inspection before making a final decision.