What’s happening in the U.S. housing market feels like a slow-moving crisis. Prices near record highs, mortgage rates above 6%, and affordability at a generational low. Yet the sharp decline most people have been bracing for still hasn’t come.

That contradiction is driving real anxiety. Buyers are holding back, and sellers are frustrated, and both want the same answer: Is the housing market going to crash in 2026, or are we stuck in this broken market indefinitely?

We break down what data is telling us. The breakdown is more nuanced than panic, and more useful than empty reassurance.

Houzeo is America’s best home buying and selling platform.

For Home Sellers: List your home for a Flat Fee, and save 2.5% to 5.5% on the listing agent commission! That’s thousands of dollars extra in your pocket.

For Home Buyers: Houzeo has the largest number of homes for sale in the US. Start your dream home search now!

Yes! You can list your home for sale or search millions of homes on the Houzeo mobile app!

Download now on the Apple App Store or the Google Play Store.

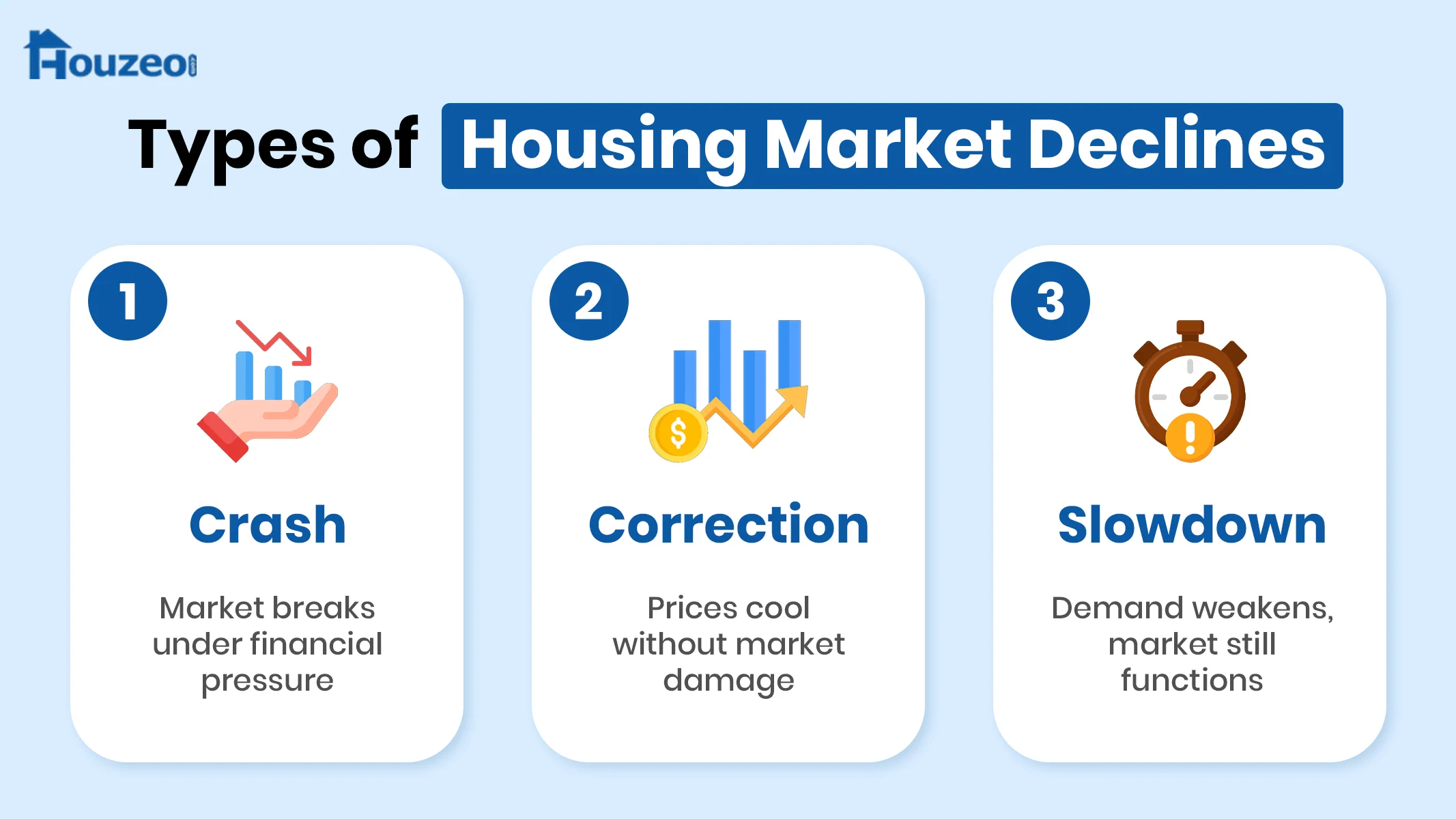

What Actually Defines a Housing Market Crash?

Not every down market is a crash. True nationwide housing crashes are extremely rare. In modern U.S. history, the last full systemic collapse happened during the 2008 housing crisis. That context matters before interpreting today’s market signals.

Prices falling alone do not create a crash. The broader financial structure matters. A housing market crash happens when several conditions combine at the same time:

- Forced selling accelerates

- Foreclosures rise rapidly

- Credit availability tightens sharply

- Buyer demand collapses

- Excess inventory floods the market

A correction is different. Prices normalize, inventory loosens, and demand cools while the market adjusts, slowly and unevenly, without breaking. A slowdown is milder, but sales volume still drops, and the price growth also stalls. The combination keeps the market functioning.

Note: The 2008 housing crisis wasn’t caused by falling home prices alone. Multiple parts of the housing and financial system broke at the same time, turning a downturn into a nationwide collapse. You should understand that not every decline leads to a crash in the market.

Why So Many Americans Think a Housing Crash Is Coming

The fear isn’t irrational. It’s built from real numbers. Since the pandemic, median home prices have risen by over 45%. Monthly mortgage payments on a median-priced home have nearly doubled. Americans are now spending around 30% of their income on housing, a record high.

Harvard’s Joint Center for Housing Studies calls affordability the worst it’s been in modern history. When a market feels that distorted, it’s natural to expect prices to eventually fall.

The memory of the 2008 US housing crisis still shapes how Americans view the market. Millions watched home values collapse, credit freeze, and foreclosures surge. So when sales slow or prices soften, many immediately fear another crash.

Housing Market 2026: Where Things Actually Stand

Home price growth is running at roughly 1% annualized as of early 2026. This is a major shift from the double-digit appreciation rates seen during the pandemic housing boom.

Inventory is expanding, and more homes are hitting the market than at any point since 2020. But nationally, supply is still below the levels that historically define a true buyer’s market.

Consumer prices jumped from 2.4% to 3.3% in March 2026. That’s keeping the Fed cautious and pushing meaningful rate relief further out.

Mortgage Rates and the Lock-In Effect

The lock-in effect is one of the main reasons the market is frozen rather than falling. Rates are sitting in the 6.3–6.5% range. Painful for buyers, but creating an equally important problem on the supply side.

Higher borrowing costs reduced affordability for buyers, but this also discouraged existing homeowners from selling. Millions of Americans locked in mortgage rates below 3% between 2020 and 2022. Selling today often means replacing those loans with rates that are more than double.

Is There a Housing Bubble Right Now?

A real estate market bubble requires three things working together: overvaluation, speculative demand, and unsustainable debt. Overvaluation is clearly present in many markets. Home prices remain elevated relative to local incomes across much of the country.

However, speculative demand looks far weaker than it did during the mid-2000s housing boom. Buyers are not aggressively chasing homes under the assumption that prices can only rise. In many areas, demand has slowed because monthly payments have become unaffordable.

Unsustainable debt at scale? Not in the way 2008 required. Post Dodd-Frank Act lending standards are significantly tighter. The subprime pipeline that fueled the last collapse doesn’t exist in the same form today. The market may be expensive, but across the US, the structure still differs from a classic speculative bubble.

Has the Housing Market Slowed Down?

Yes, clearly. Across much of the country, the housing market has already slowed considerably. So, are housing prices dropping as well? In certain metros, yes. Homes aren’t selling as quickly as they were a few years ago, and price growth has cooled noticeably.

Why the Housing Market Is Unlikely to Crash?

Several structural conditions continue to reduce the probability of a nationwide collapse.

1. No forced selling at scale. Most homeowners are sitting on significant equity built during the pandemic run-up. Unlike 2008, relatively few borrowers are deeply underwater on their mortgages. There’s no financial pressure forcing them to sell at any price. Without forced selling, there’s no panic spiral.

2. Lending standards are tight. The Dodd-Frank Act reshaped mortgage lending after 2008. The reckless loan products that created the financial crisis are largely gone from the mainstream market. Lenders now verify income, assets, and debt ratios in ways they simply didn’t before.

3. Inventory growth remains gradual. Crashes usually require large amounts of distressed supply arriving quickly, but the national inventory trends still do not reflect that pattern.

4. The labor market is still relatively stable. Job loss is the primary spark for the flame called forced selling. While layoffs have increased in some sectors, national labor conditions have not deteriorated enough to create broad mortgage distress.

All of these indicators are showing that instead of asking if the housing market will crash, you should focus on whether housing will become affordable soon enough or not.

Risks in the Housing Market

Although the chances are low, some of the factors that will drive the upcoming housing crash, if it materializes, are as follows.

- Labor Market Deterioration: AI-related layoffs are wrecking the job market, and the damage done by the DOGE is still affecting employment, especially in the public sector.

- Insurance and Tax Pressure: In markets like Florida and coastal Texas, people are paying higher insurance premiums to protect against climate disasters such as hurricanes, floods, and extreme winters. Property taxes are also increasing.

- Aging Boomer Inventory: More Baby Boomers are now part of the estate and downsizing phase. If that volume accelerates in specific local markets, it adds real supply pressure there.

- Localized Oversupply: Some Sun Belt metros like Austin expanded aggressively during the pandemic migration boom and are already experiencing softer pricing trends.

What Experts Are Forecasting for 2026

A major prediction on the housing market is pointing towards normalization and not collapse. Zillow’s latest 2026 forecast projects 0.6% home value appreciation for the ~1.23 million existing home sales for the year. House Prices are following a steady line and not a sharp decline.

Redfin Chief Economist Daryl Fairweather describes the current market as a “long-term correction, not a crash.” The broader consensus is relatively consistent:

- Regional differences will matter far more than national averages

- Price growth likely remains slow

- Mortgage rates may ease gradually rather than sharply

- Inventory should continue improving incrementally

What Happens If the Housing Market Crashes?

Housing market drop is being talked about out there, but a crash is unlikely. However, if it does happen, almost all stakeholders of the market will be affected.

- Homeowners could see their equity shrink or even turn negative if home values fall significantly. Refinancing becomes harder, and selling often means realizing a financial loss.

- Buyers face a different issue in the crash. Homes for sale prices do take a hit, but at the same time, banks tighten lending standards to prevent inflation. Homes may become cheaper while financing becomes more difficult to secure.

- Prices drop, which leaves sellers with less negotiating power. Houses take longer to sell, which leaves sellers with a binary: to not sell or to sell at a loss.

- If investors have strong liquidity or very strong existing credit, they rush to take advantage of the distressed opportunities. Meanwhile, ordinary buyers suffer the most.

Should You Wait for a Crash Before Buying?

Many buyers have delayed home purchases since 2022, but prices haven’t seen a sharp decline yet. However, this wait also works against buyers. Every month of waiting is a month of rent paid instead of equity built.

Currently, buyers do have advantages like increased inventory, less competition, and longer decision timelines. You should think about what you can buy instead of worrying about a possible collapse, and explore different homes for sale.

» Houzeo Reviews: Read what customers have to say about Houzeo, America’s best home buying website.